Online ITR Filing in India 2026: Complete Step-by-Step Guide

Nowadays, filing Income Tax Return (ITR) has become one of the most important financial responsibilities for taxpayers in India. Whether you are a salaried employee, freelancer, consultant, startup founder, or business owner, filing your ITR correctly helps you stay compliant with tax laws and avoid future financial issues.

With the growth of digital services, Online ITR Filing in India 2026 has become faster, easier, and more convenient than ever before. Taxpayers can now complete the entire Income Tax Return Filing process online without visiting any office physically.

However, many people still get confused about choosing the correct ITR form, selecting the right tax regime, claiming deductions, checking AIS records, and filing returns properly. This complete guide will help you understand the entire Online ITR Filing process step by step.

What is Online ITR Filing?

Online ITR Filing is the process of submitting your Income Tax Return electronically through the Income Tax Department portal. Taxpayers can report their income, deductions, taxes paid, and refund claims digitally.

Today, Income Tax e-Filing in India is preferred because it is:

- Faster

- Paperless

- Secure

- Easy to track

- Convenient

Online filing also helps the government process refunds more quickly and efficiently.

Who Should File Income Tax Return in 2026?

Many people think only high-income individuals need to file ITR. However, filing income tax returns is important for several categories of taxpayers.

You should file ITR if:

- Your income exceeds the exemption limit

- TDS has been deducted from your income

- You want to claim a tax refund

- You are a freelancer or business owner

- You have foreign income or assets

- You need financial proof for loans or visas

Even individuals with low taxable income often file returns for financial documentation and future benefits.

Benefits of Online ITR Filing

1. Faster Processing

Online returns are processed much faster than offline filing methods.

2. Easy Refund Tracking

Taxpayers can easily track refund status online.

3. Better Accuracy

Digital systems reduce manual mistakes and calculation errors.

4. Convenient Filing

Returns can be filed anytime from home without visiting tax offices.

5. Financial Proof

ITR acts as important income proof for:

- Bank loans

- Credit cards

- Visa applications

- Business funding

Documents Required for Online ITR Filing

Before starting the ITR Filing Process 2026, keep the required documents ready.

For Salaried Employees

- PAN Card

- Aadhaar Card

- Form 16

- Salary slips

- Bank statements

- Investment proofs

- Home loan documents (if applicable)

For Freelancers

- Income records

- Expense details

- GST information

- TDS certificates

- Bank statements

For Business Owners

- Financial statements

- Profit and loss account

- Balance sheet

- GST returns

- Audit reports (if applicable)

Keeping proper documents ready helps reduce mistakes during filing.

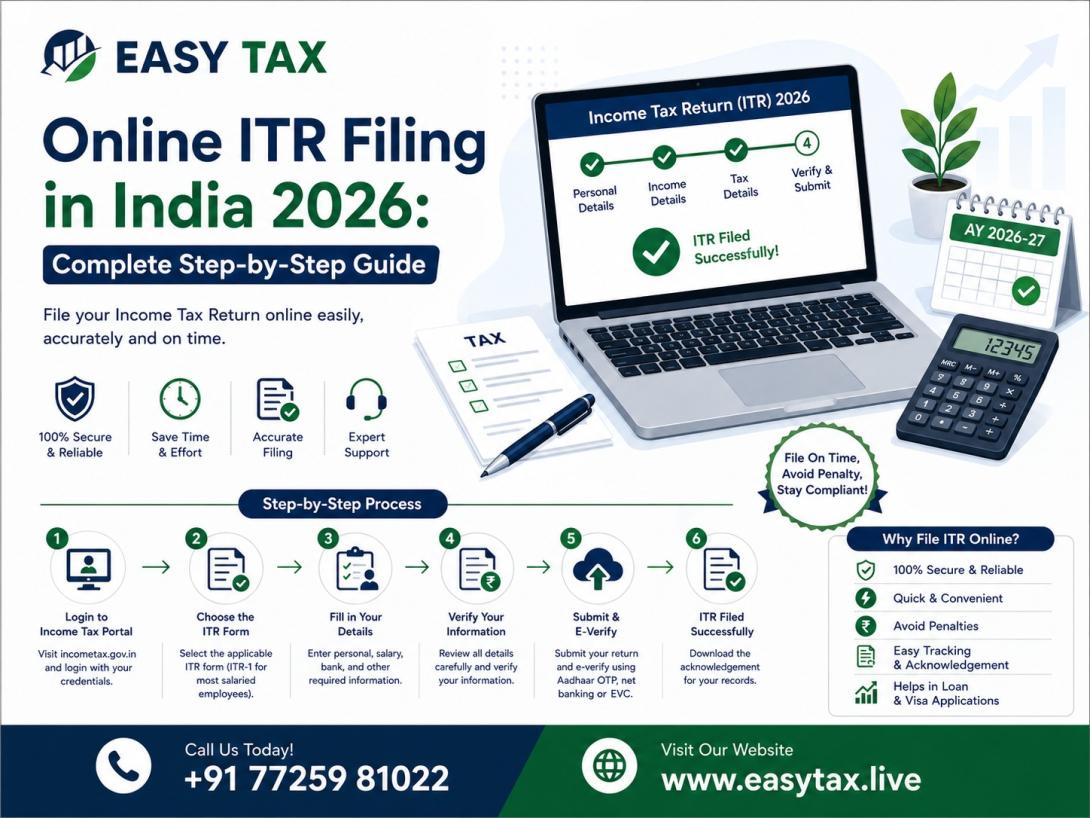

Step-by-Step ITR Filing Guide 2026

If you are wondering how to file ITR online, follow this simple process.

Step 1: Visit the Income Tax Portal

Go to the official Income Tax e-filing portal and log in using:

- PAN number

- Password

- Aadhaar-linked OTP

First-time users must complete registration before filing.

Step 2: Choose the Correct ITR Form

Selecting the correct ITR form is extremely important.

Common ITR forms include:

- ITR-1 – Salaried individuals

- ITR-2 – Capital gains or multiple income sources

- ITR-3 – Business or professional income

- ITR-4 – Presumptive taxation scheme

Using the wrong form may lead to defective return notices.

Step 3: Select Tax Regime

Taxpayers now have two tax regime options:

- Old Tax Regime

- New Tax Regime

The old regime allows deductions and exemptions, while the new regime offers lower tax rates with fewer deductions.

Choosing the correct regime is one of the most important tax filing decisions.

Step 4: Enter Income Details

Carefully enter all sources of income, including:

- Salary income

- Bank interest

- Rental income

- Freelance income

- Capital gains

- Business income

Always match your details with AIS and TIS records to avoid future notices.

Step 5: Claim Deductions

Under the old tax regime, taxpayers can claim deductions such as:

- Section 80C investments

- Health insurance under 80D

- Home loan interest

- HRA exemption

- NPS contributions

Proper deduction claims help reduce taxable income legally.

Step 6: Verify Taxes Paid

Check details of:

- TDS deducted

- Advance tax paid

- Self-assessment tax

These details are available in Form 26AS.

Step 7: Submit and Verify Return

After reviewing all information:

- Submit the return online

- Complete e-verification using Aadhaar OTP, net banking, or bank verification

Without verification, your return remains incomplete.

Online ITR Filing for Salaried Employees

Online ITR Filing for Salaried Employees is generally simpler, but mistakes are still common.

Common filing issues include:

- Incorrect HRA claims

- Multiple Form 16 confusion

- Missing bank interest income

- Wrong tax regime selection

Professional guidance can improve accuracy and reduce errors.

ITR Filing for Freelancers

Freelancers often face additional tax complications because of:

- Multiple clients

- Online payments

- Foreign income

- GST compliance

- Expense claims

Freelancers should properly maintain:

- Invoices

- Expense bills

- Bank statements

- TDS records

Accurate bookkeeping helps simplify tax filing and avoid notices.

Common Mistakes During Online ITR Filing

Many taxpayers make avoidable errors while filing returns themselves.

Choosing Wrong ITR Form

Using the incorrect form may trigger notices.

Missing Income Sources

Taxpayers often forget to report:

- Savings account interest

- FD interest

- Freelance income

- Capital gains

Incorrect Deduction Claims

Claiming ineligible deductions may lead to scrutiny.

Ignoring AIS and TIS

Mismatch between filed data and government records can create compliance issues.

Filing After Deadline

Late filing may result in penalties and interest charges.

Online ITR Filing for Beginners

For first-time taxpayers, online filing may initially look confusing. However, the process becomes much easier when you:

- Keep documents ready

- Understand your income sources

- Select the correct tax regime

- Verify details carefully

Beginners should avoid rushing during filing season.

Why Many Taxpayers Prefer Online CA Services for ITR Filing

As taxation becomes more technical, many individuals now prefer professional online CA services.

Professional tax experts help with:

- Accurate filing

- Deduction optimization

- Tax planning

- Notice handling

- Tax regime comparison

This helps reduce stress and improves filing accuracy.

Best Income Tax Filing Tips 2026

Keep Documents Organized

Maintain salary slips, investment proofs, and bank statements properly.

File Before Deadline

Avoid penalties and late fees.

Match AIS and Form 26AS

Always reconcile your records before filing.

Compare Tax Regimes

Calculate taxes under both regimes before choosing one.

Take Professional Help

Professional guidance can help maximize tax savings legally.

Why Online Tax Filing in India is Growing Rapidly

Digital taxation systems have completely transformed tax filing in India. Taxpayers now prefer online filing because it offers:

- Convenience

- Faster processing

- Transparency

- Secure filing

- Easy refund tracking

Easy online filing has made tax compliance more accessible than ever.

Conclusion

Online ITR Filing in India 2026 has made income tax return filing easier, faster, and more convenient for taxpayers. Whether you are a salaried employee, freelancer, consultant, or business owner, understanding the filing process is extremely important for smooth compliance.

By following this step-by-step guide, keeping proper documents ready, and selecting the correct tax regime, taxpayers can complete their Income Tax Return Filing 2026 accurately and avoid common filing mistakes.

If you find taxation confusing, taking professional help from experienced tax consultants or CA services can save time, reduce stress, and improve filing accuracy. Proper tax filing is not only a legal responsibility but also an important part of smart financial planning.